Credit card bills can be confusing, especially when terms like “FPV” appear. Many cardholders struggle to understand what they owe and when. This lack of clarity often leads to missed payments, late fees, and damaged credit scores.

Full Payment Value (FPV) is a crucial concept that can help you manage your credit card debt more effectively. By grasping it, you’ll gain control over your finances and avoid costly mistakes. This guide will explain FPV in simple terms, show you how to calculate it, and provide tips for using this information to your advantage.

Defining FPV What Does It Really Mean?

FPV stands for Full Payment Value. It’s the amount you need to pay to clear your credit card balance. This includes your purchases, interest, and fees. Understanding it helps you manage your credit better. It’s a key part of your credit statement. Knowing your full payment value can help you avoid debt.

The Significance of FPV in Credit Reports

It shows up on your credit report. It tells lenders how much you owe. A high full payment value might make getting new credit harder. Lenders use it to judge your financial health. Keeping it low can improve your credit score. It’s a sign you’re handling credit well.

Demystifying FPV on Credit

It is simpler than it sounds. It’s just the total you need to pay off. This includes all charges on your card. Knowing your FPV helps you plan your budget. It shows the real cost of your credit card use. Understanding it can help you make better spending choices.

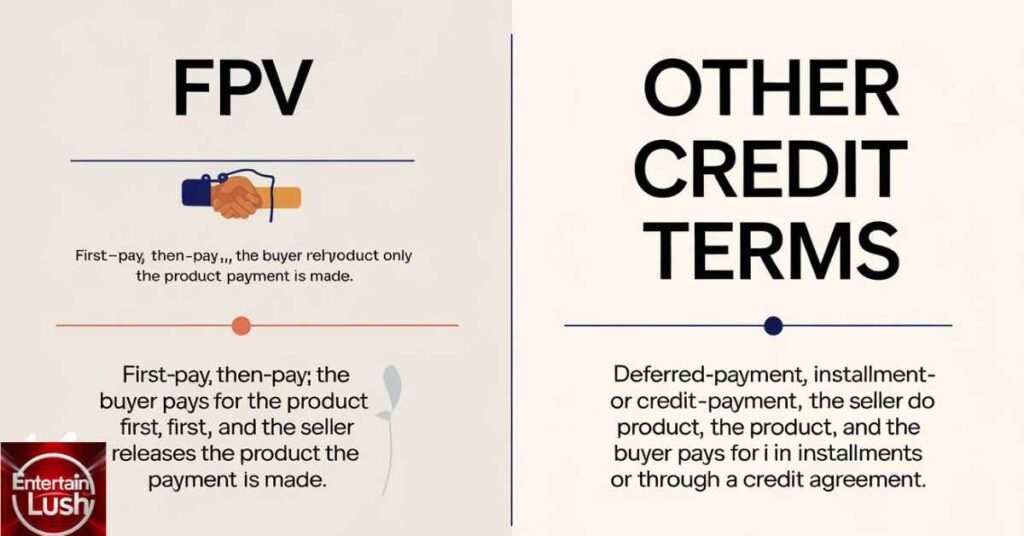

FPV vs. Other Credit Terms: Key Differences

It is different from your credit limit. Your limit is how much you can spend. It is how much you owe. It’s also not the same as your current balance. Your balance might not include recent interest or fees. It gives a more complete picture of your debt.

The Evolution of FPV in Credit Reporting

FPV became important in the 1970s. It hasn’t always been a big deal in credit reports. Let’s look at how it changed over time! In the 1990s, credit reports were simpler. They didn’t use FPV. People just looked at how much you owed. By 2005, things started to change.

Banks wanted more info about spending habits. That’s when this payment value started to show up. In 2010, it became more common. But many people still didn’t understand it. Now, in 2024, it is super important. It helps show how you use your credit cards each month. Over the years, this payment value has become a key part of your credit score.

It’s funny to think it wasn’t always this way! That’s when credit cards became popular. Banks needed a way to show total debt. It filled this need. Over time, it became a standard credit term. Now, it’s a key part of credit reports and financial planning.

The Calculation of FPV

To find your FPV, add up all charges. This means purchases, cash advances, and balance transfers. Then add interest and fees. The total is your FPV. Card companies do this math for you. They show it on your statement. It’s the amount you need to pay to clear your balance.

Components of FPV: What’s Included?

It includes several parts. First, there’s your main balance from purchases. Then, any cash advances you’ve taken. Balance transfers are also part of it. Don’t forget interest charges. Lastly, add any fees you’ve been charged. All these make up your FPV. Here’s a simple table showing FPV calculation examples:

| Item | Amount |

| Purchases | $500 |

| Cash Advance | $100 |

| Interest (2%) | $12 |

| Cash Advance Fee | $5 |

| Total FPV | $617 |

This table breaks down the FPV calculation. It shows each part clearly. You can see how different charges add up. The total at the bottom is your Full Payment Value. This is what you’d need to pay to clear your balance completely. Tables like this can help you understand your credit card statement better.

The Impact of FPV on Your Credit Score

Your full payment value affects your credit utilization. This is a big part of your credit score. A high FPV compared to your credit limit can lower your score. Keeping it low shows you use credit responsibly. This can help improve your credit score over time. Lenders like to see a low FPV.

Credit Utilization and FPV A Crucial Relationship

It directly affects your credit utilization ratio. This ratio is how much credit you’re using compared to your limit. A lower ratio is better for your credit score. For example, if your credit limit is $1000 and your FPV is $300, your utilization is 30%. Keeping this under 30% is generally good for your credit health.

FPV and Credit Score Models FICO and Vantage Score

FICO and Vantage Score look at your full payment value differently. Both care about how much you owe. FICO focuses more on your payment history. Vantage Score pays more attention to recent credit use. Both see a high FPV as risky. Keeping it low helps with both types of credit scores.

Strategies for Managing Your Full Payment Value

Pay more than the minimum each month. This lowers your FPV faster. Try to pay in full when you can. Use your card less if your full payment value is high. Check your balance often. This helps you avoid overspending. Set up alerts for when your balance gets high. Planning your spending helps keep FPV low.

Timing Your Payments Optimizing FPV Impact

When you pay matters. Paying before your statement date lowers your reported FPV. This can help your credit score. Even if you can’t pay in full, paying early helps. It reduces the balance that gets reported. Try to pay something weekly if you can. This keeps your FPV lower.

Balancing Multiple Credit Accounts FPV Considerations

Having many credit cards and loans can be tricky. You need to keep an eye on all of them. It’s like juggling – you don’t want to drop any balls! Think about how much you owe on each card. Try to pay off the ones with high interest first. This helps you save money in the long run.

Full Payment Value and Credit Card Rewards

It’s the amount you need to pay to avoid interest on your credit card. Many cards offer rewards like cash back or points when you spend money. But here’s the trick: these rewards are only good if you pay your full balance. If you don’t pay the full payment value, the interest can cost more than the rewards you earn.

How FPV interacts with credit card reward programs

Paying it every month helps you get the most from your card’s rewards. Let’s say you get 2% cash back on purchases. If you always pay the full amount, you’re really saving 2%. But if you only pay part and get charged interest, you might end up losing money instead. So, try to pay the full amount to make those rewards count!

Maximizing Rewards Without Inflating FPV

Want to get more rewards without spending too much? It’s possible! Use your card for things you’d buy anyway, like groceries or gas. Look for special deals where you can earn extra points. But remember, only spend what you can pay off each month. This way, you get rewards without growing your debt. It’s like getting a little bonus for being smart with your money.

Strategies for earning rewards while maintaining a healthy FPV

Try these tricks: Use your card for all your regular bills. Join your card’s special programs for extra points. But always keep track of what you’re spending. Set a budget and stick to it. This helps you earn rewards while keeping your balance low. It’s like walking a tightrope – stay balanced and you’ll do great!

The FPV Trap When Chasing Rewards Backfires

Sometimes, trying to get lots of rewards can backfire. You might spend more than you planned just to get points. This can make it (the amount you owe) go up fast. If you can’t pay it all off, you’ll end up paying interest. That interest can cost more than the rewards are worth. It’s like running after a shiny object and falling into a hole!

Potential pitfalls of focusing too much on rewards at the expense of FPV

Watch out for these dangers: Spending more than you can afford just to get rewards. Forgetting about the interest you’ll owe if you don’t pay in full. Signing up for too many cards and losing track of payments. Remember, rewards are only good if you’re not in debt. Don’t let the promise of points lead you into financial trouble.

FPV and Credit Limit Management

Your credit limit affects your full payment value’s impact. A higher limit can make the same payment value look better. For example:

| Credit Limit | Full Payment Value | Utilization |

| $1,000 | $300 | 30% |

| $2,000 | $300 | 15% |

In 2024, managing your credit limit is key to keeping a healthy credit profile. A lower utilization generally means a better credit score.

Requesting Credit Limit Increases FPV Implications

Asking for a higher credit limit can be good. It can lower your credit use if you don’t spend more. But be careful! A higher limit might tempt you to spend more. This could make your full payment value go up. Remember, a bigger credit jar doesn’t mean you should fill it up. Keep your spending the same, and you’ll be in good shape.

Optimal Credit Utilization Finding the FPV Sweet Spot

The sweet spot for credit use is using about 30% or less of your limit. This means if your limit is $1000, try to keep your FPV under $300. It’s like filling your plate at a buffet – don’t overfill it! This balance looks good to the credit score folks. It shows you can use credit without maxing it out.

The Role of FPV in Lending Decisions

When you ask for a loan, lenders look at your full payment value. They want to see if you pay your bills on time. If your full payment value is always low, it’s a good sign. It shows you’re responsible with money. Lenders like that! It’s like showing them you always clean your room – they’ll trust you more.

Read This Blog: Hidden Gems in TotallyNDFW: Your Ultimate Guide to Undiscovered Treasures

FPV Analysis What Lenders See

Lenders check your full payment value history. They see how much you owe and if you pay on time. They look for patterns. Do you max out your cards? Do you pay in full? It’s like they’re reading a story about how you use money. They use this to decide if they want to lend to you.

Also Read: Emma Coleman Latta’s Impact on South Carolina: A Hidden Historical Gem

Improving Your FPV Profile for Better Loan Terms

To get better loans, keep your FPV low. Pay your bills on time, every time. Don’t use all your credit. If you have high balances, try to pay them down. It’s like cleaning up your room before your parents check it. A tidy FPV profile can help you get better deals on loans.

FPV and Financial Planning

Think about it when you plan your money. It’s part of the big picture. Keep track of what you owe. Plan how you’ll pay it off. This helps you avoid surprises. It’s like including snacks in your meal plan – don’t forget about it! Good FPV management makes your whole money plan stronger.

Budgeting with Full Payment Value in Mind

When you make a budget, think about your FPV. Plan to pay more than the minimum on your cards. Set aside money for this every month. It’s like saving for a trip – a little bit often adds up! This helps keep it low and your credit score happy.

Long-Term Financial Goals and FPV Management

It affects your big-money goals. Want to buy a house? Save for retirement? A low FPV helps with these. It means less debt and more savings. Think of its management as part of your future planning. It’s like planting a money tree – take care of it now, and it’ll help you later!

FAQ

What is FPV?

FPV stands for Full Payment Value. It’s the total amount you need to pay on your credit card to avoid interest charges.

Is FPV the same as my credit limit?

No, FPV and credit limit are different. Your credit limit is how much you can spend, while full payment value is how much you currently owe.

How often is my FPV updated?

It usually updates daily as you make purchases or payments. However, it may take a day or two for changes to appear on your statement.

Does FPV affect my credit score?

Yes, FPV can affect your credit score. A high FPV compared to your credit limit can lower your score.

Does FPV include pending transactions?

Usually, it doesn’t include pending transactions. It only includes charges that have been fully processed and posted to your account.

Conclusion

Managing your FPV is key to good credit health. It’s like keeping your piggy bank in check. Pay attention to how much you owe and try to pay it off each month. This helps you avoid extra costs and keeps your credit score happy.

Remember, rewards are nice, but not if they lead to more debt. Use your credit cards wisely, like tools to build a better financial future. With some care and smart choices, you can make FPV work for you, not against you.

Mr. Dravid is the dedicated author of the business category on Entertainlush.com. With a keen eye for industry trends and a passion for insightful analysis, he delivers valuable content that empowers readers to stay ahead in the ever-evolving business landscape. His expertise ensures that every article is both informative and engaging, helping audiences navigate the complexities of the business world.